For all the discussion about the Bangladesh’s recent economic woes, the declining exports has not received much attention. However, exports have been weak for a while now, with possibly significant consequences for the broader economy. This post is a preliminary investigation into the issue.

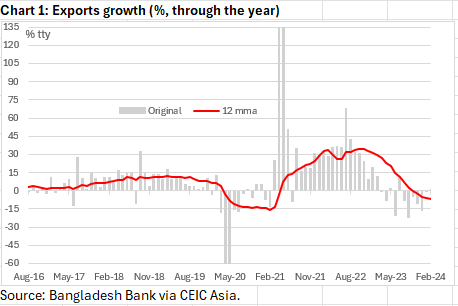

Exports declined on a year-ended basis in seven months of 2023 as well as in the year to January 2024. Monthly exports data is volatile, not to mention the wild swings during the pandemic, and it is a standard practice to smooth the series. Chart 1 shows the through the year (or year-ended growth) in both the original and smooth (12 month moving average) series. It is clear that exports have been weak for nearly a year.

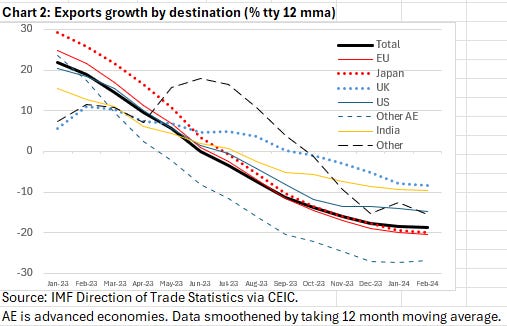

Chart 1 uses Bangladesh Bank data where exports receipts are reported in taka. Chart 2 uses the IMF Direction of Trade Statistics, which reports exports in US dollar and breaks it down by destination countries. It is clear that exports have been weak for many months now, and the weakness is to all destinations.

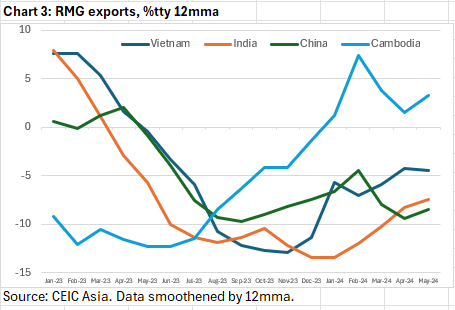

Since most of Bangladesh’s exports are readymade garments, the reasons behind the exports weakness would likely be in that sector. If there is something global going on, this should show up in exports data of other countries. And Chart 3 suggests that this is indeed the case. Exports of RMG products have been declining in Vietnam, India and China, though it seems to be recovering in Cambodia.

That is, domestic factors — such as labour unrest, electricity shortage, fear of sanctions in 2023 — may have contributed to the weakness in Bangladeshi exports, but the more important story is probably global.

One possibility is that western consumers, in face of inflation and rising interest rates, maybe cutting back on their purchase of garments. Another possibility is that there is something structural going on in the global garments supply chain — such as the advent of online shopping at the expense of retail outlets. Production could be moving to Cambodia and other countries, and away from Bangladesh, Vietnam, China and India. Of course, these and other factors may be linked.

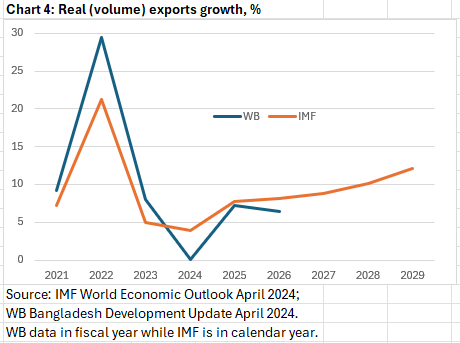

This needs to be explored in much more depth. For now, however, one solace is that both the World Bank and the IMF are projecting a recovery in real (volumes) exports in the medium-term (Chart 4) — that is, their current analysis is not one of structural shifts in the industry.

Regardless of the underlying cause, the exports weakness must have

had flow on effects. Given the popular fascination with the stock of

foreign reserves, it might be tempting calculate what declining exports

mean for the balance of payments. However, such mechanical calculations

actually miss the more significant macroeconomic linkages. At the very

least, the economy has been hit with a negative exports shock in recent

months.

The exports decline is probably related to the slowdown in industrial production (Chart 5). Meanwhile, the RMG sector is likely facing a squeeze on its profits even as the workers’ are reeling from cost of living pressures and have been agitating for higher wages. The income loss could flow through to weakening household consumption, dragging GDP growth down even further (it has already been slowing in the second half of 2023).